JOINT PRESS RELEASE

This is a joint press release by Koninklijke Ten Cate N.V. ("TenCate" or "the Company") and Tennessee Acquisition B.V. (the "Offeror") pursuant to the provisions of Section 4, paragraphs 1 and 3 and Section 5, paragraph 1 and Section 7, paragraph 4 of the Netherlands Decree in Public Takeover Bids (Besluit openbare biedingen Wft, (the "Decree") in connection with the intended public offer by the Offeror for all the issued and outstanding ordinary shares in the capital of TenCate (the "Shares"). This announcement does not constitute an offer, or any solicitation of any offer, to buy or subscribe for any securities in TenCate. Any offer will be made only by means of an offer memorandum (the "Offer Memorandum"). This announcement is not for release, publication or distribution, in whole or in part, in or into, directly or indirectly, Canada and the United States.

20 July 2015

GILDE BUY OUT Partners leads consortium to make a recommended cash offer for all shares of TenCate

Consortium supports the current strategy of TenCate

Transaction highlights

TenCate and Tennessee Acquisition B.V., a company controlled by a consortium of investors led by Gilde Buy Out Partners and also including Parcom Capital and ABN Amro Participaties (the "Consortium") have reached a conditional agreement on a full public offer of EUR 24.60 (cum dividend) in cash per ordinary share of TenCate (the "Offer Price")

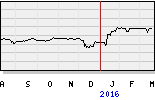

The Offer Price represents a premium of 26.8% to the closing price of 17 July 2015 and a premium of 27.1% to the average closing price for the 12 months prior to and including that date

The Executive Board and the Supervisory Board of TenCate fully support and unanimously recommend the Offer

Funds managed by Delta Lloyd have irrevocably undertaken to support and accept the Offer. In addition, Mr. Loek de Vries, President and CEO of TenCate, has also irrevocably agreed with the Offeror that, provided TenCate continues to recommend the Offer, he will support and accept the Offer. These irrevocable commitments together represent approximately 16% of all issued and outstanding Shares

The Offeror has committed financing in place, providing a high level of deal certainty

Strategic rationale

Full support for TenCate's long-term growth strategy, including potential acquisitions

Consortium composed of experienced Dutch based investors with long-term investment focus well placed to provide TenCate with strong financial backing, expertise and support to realise its full potential

Consortium aims to secure continued leadership for TenCate in its core specialty niches across its five market groups

Non-financial terms

Corporate identity and culture of TenCate maintained

TenCate headquarters, central management and key support functions remain in Almelo

No reorganisation or restructuring plan resulting in significant job losses as a direct consequence of the Offer

Existing rights and benefits of the employees of TenCate will be respected

Almelo/Utrecht, 20 July 2015 - Royal Ten Cate N.V. and Tennessee Acquisition B.V., a company controlled by a consortium of investors led by Gilde Buy Out Partners and also including Parcom Capital and ABN Amro Participaties, today jointly announce that they have reached conditional agreement on an intended recommended full public offer for TenCate of EUR 24.60 (cum dividend) in cash per ordinary share of TenCate, subject to customary conditions (the "Offer"). The Offer Price represents a premium of 26.8% to the closing price of 17 July 2015, and a premium of 27.1% to the average closing price for the 12 months prior to and including that date.

Loek de Vries, President and Chief Executive Officer of TenCate, said: "This offer represents positive news for all stakeholders involved in our company. Both our employees and our customers will benefit from the longer-term horizon the consortium will bring. There is a clear commitment to support our strategy, which means we can invest in our product-market-technology combinations, thereby further strengthening our leading market positions. In addition, we can continue our buy and build approach and we will benefit from the capabilities, experience and financial support of our new shareholders. Last but not least, the offer represents a fair price for our existing shareholders. The boards consider the offer to be in the best interest of TenCate and we therefore fully support and unanimously recommend the offer".

Hein Ploegmakers, Partner at Gilde said: "The Consortium has great respect for the longstanding heritage of TenCate covering over 300 years of history. TenCate's market groups hold leadership positions in a number of high growth, specialised niche markets and we aim to support each of them the best we can. Together with our co-investors Parcom Capital and ABN Amro Participaties, we are delighted at the prospect of working with TenCate management and supporting them in the next stage of the Company's development."

Strategic rationale

TenCate considers this intended transaction to be a compelling Offer for all the Company's stakeholders.

The combination of the Offeror and TenCate will help the TenCate group (the "Group") realise its business strategy, allowing it to improve and invest in the existing five market groups (Protective Fabrics, Advanced Composites, Advanced Armour, Geosynthetics and Grass) and, as part of an effective buy & build strategy, to strengthen these market groups further through acquisitions.

With a focussed shareholder consortium as its controlling shareholder base, TenCate will have ample access to liquidity for long term value enhancement of the business. This focus on value creation will also benefit commercial relationships through product development and innovations.

The Consortium will bring extensive experience and a strong track record of supporting management teams in the execution of their business plans. The members of the Consortium have a clear understanding of the markets in which the Group operates.

Support and recommendation from the Executive Board and the Supervisory Board

Throughout the process, TenCate's executive board (the "Executive Board") and supervisory board (the "Supervisory Board", and together with the Executive Board the "Boards") have met on a frequent basis to discuss the progress of the discussions with the Offeror and the key decisions in connection therewith.

The Boards have received extensive financial and legal advice and have given careful consideration to all aspects of the Offer, including strategic, financial, operational and social points of view.

After due and careful consideration, both the Executive Board and the Supervisory Board are of the opinion that the Offeror makes a compelling Offer representing a fair price and attractive premium to TenCate's shareholders, as well as favourable non-financial terms. The Boards consider the Offer in the best interest of TenCate and all its stakeholders, also including employees, governmental organisations, customers, suppliers and R&D partners.

Rabobank has issued a fairness opinion to the Executive Board and the Supervisory Board, and NIBC Bank has issued a fairness opinion to the Supervisory Board. Both have opined that the Offer Price is fair, from a financial point of view, to the shareholders.

Taking all these considerations into account, both the Executive Board and the Supervisory Board fully support and unanimously recommend the Offer for acceptance to the Shareholders.

A steering committee comprising the members of the Executive Board and certain members from the Supervisory Board together with TenCate's financial and legal advisors ("Steering Committee") was formed at the start of the process. The Steering Committee reviewed the indicative offer and discussed the terms of the Offer with the Offeror.

During the process, a potential conflict of interest arose in relation to one member of the Supervisory Board, Mr. Egbert ten Cate. Mr. Ten Cate then withdrew from the Steering Committee and did not participate in the discussions and decision-making process regarding the Offer within the Supervisory Board. Once the members of the Executive Board started discussing terms of continued involvement after settlement of the Offer with the Offeror, they withdrew from the Steering Committee and no longer participated in the negotiations of a conditional agreement with the Offeror regarding the Offer.

Irrevocable undertakings, investment by Board members

Delta Lloyd Deelnemingen Fonds N.V., Delta Lloyd Levensverzekeringen N.V. and Delta Lloyd L European Participation Fund have irrevocably undertaken to support and accept the Offer. In addition, Mr. Loek de Vries, President and CEO of TenCate, has also irrevocably agreed with the Offeror that, provided TenCate continues to recommend the Offer, he will support and accept the Offer. These irrevocable commitments together represent approximately 16% of all issued and outstanding Shares.

In accordance with the applicable public offer rules, any information shared with these major shareholders about the Offer shall, if not published prior to the Offer Memorandum being made generally available, be included in the Offer Memorandum in respect of the Offer (if and when issued) and these major shareholders will tender their Shares on the same terms and conditions as the other shareholders.

In addition, Mr. Loek de Vries, President and CEO of TenCate, has agreed with the Offeror that he will invest part of the proceeds of the Offer received by him in his capacity as TenCate shareholder in the capital of an affiliate of the Offeror following settlement of the Offer.

Furthermore an investment company of the Ten Cate family has agreed with the Offeror to invest in the capital of an affiliate of the Offeror following settlement of the Offer.

Corporate governance

TenCate and the Offeror have agreed that following settlement of the Offer, TenCate will continue to voluntarily apply the mitigated structure regime for large companies (gemitigeerd structuurregime).

The Supervisory Board will comprise of five members of which three new members will be nominated by the Offeror. The two continuing members of the Supervisory Board will need to remain independent as meant in the Dutch Corporate Governance Code until the earlier of (i) three years after the settlement date of the Offer, and (ii) the moment that TenCate no longer has any minority shareholders. Mr Jan Hovers and Mr Egbert ten Cate will continue as member of the Supervisory Board following settlement of the Offer (the "Continuing Members").

The current members of the Executive Board shall upon settlement of the Offer continue to serve as members of the Executive Board.

Non-financial covenants

The Offeror values the interests of all stakeholders of TenCate, including shareholders, employees, governmental organisations, customers, suppliers, R&D partners and others, and recognises the corporate identity of TenCate based on a legacy built up over more than three centuries. Therefore, the Offeror has agreed certain non-financial covenants with regard to the strategy, structure and governance, financing, minority shareholders, employees, as well as other matters, including that:

TenCate will remain a separate legal entity and will remain the holding company of the Group and its operations from time to time, with headquarters, central management and key support functions in Almelo

the "TenCate" brand will remain a key aspect of TenCate's branding and marketing strategy

the Group will remain prudently financed to safeguard the continuity of the business and the execution of the business strategy

no substantial part of the Group will be divested

in relation to employees:

the Offeror will respect and aim to maintain TenCate's culture of excellence, which requires highly talented employees and employees will be appropriately trained and provided with clear career progression

the arrangements with TenCate's works councils and relevant trade unions will be respected

the rights and benefits of the employees of TenCate's group under their individual employment agreements, collective labour agreements and social plans will be respected

the pension arrangements between TenCate and Stichting Pensioenfonds Koninklijke Ten Cate and non-Dutch pension-service providers as disclosed by TenCate to the Offeror will be respected

there will be no reorganization or restructuring plan resulting in significant job losses in any country in which TenCate operates, taking into account the total number of employees of TenCate in that country, as a direct consequence of the Offer

These non-financial covenants shall terminate three years after the settlement date of the Offer. Any deviation from these non-financial covenants prior to the third anniversary of the settlement date of the Offer requires the prior approval of the Supervisory Board, with the affirmative vote of at least one Continuing Member.

Any successor to the Offeror will be required to commit to the same non-financial covenants for any remaining part of the period to which the Offeror had committed.

Financing of the Offer

The Offer values 100% of the issued Shares at approximately EUR 675 million.

The Offeror shall finance the Offer through a combination of shareholder funding made available on behalf of the Offeror and third party debt financing. In this context the Offeror has received binding equity commitment letters including from entities managed, controlled and/or advised by each of Gilde, Parcom Capital and ABN Amro Participaties, as well an investment company of the Ten Cate family, for an aggregate amount of EUR 362.5 million, which are fully committed, subject to customary conditions (the "Shareholder Financing"). In addition the Offeror has entered into binding debt commitment papers with a consortium of reputable banks for senior debt financing in an aggregate amount of EUR 520 million of term debt and a revolving facility of EUR 75 million, which is fully committed on a "certain funds" basis, subject to customary conditions (the "Debt Financing"). The Offeror has no reason to believe that any such conditions to the Shareholder Financing or the Debt Financing will not be fulfilled on or prior to the settlement date under the Offer.

From the Shareholder Financing and the Debt Financing, the Offeror will be able to fund the acquisition of the Shares under the Offer, the refinancing of existing TenCate debt financing and the payment of fees and expenses related to the Offer.

Commencement Conditions and Offer Conditions

Commencement of the Offer is subject to the satisfaction or waiver of commencement conditions customary for a transaction of this kind, being:

(i) all competition filings having been made;

(ii) no material adverse change having occurred;

(iii) the completion of TenCate's employee co-determination procedures and other employee related notification procedures regarding all relevant aspects of the Offer (including the financing thereof);

(iv) the approval of the final draft Offer Memorandum by the Netherlands Authority Financial Markets (Stichting Autoriteit Financiële Markten, "AFM");

(v) no initial public announcement having been made of (i) a Competing Offer (as defined and briefly described below) or (ii) a mandatory offer pursuant to article 5:70 of the Dutch financial supervision act (Wet op het financieel toezicht, "Wft");

(vi) the Boards not having revoked, modified, amended or qualified their recommendation of the Offer;

(vii) no notification having been received from the AFM stating that pursuant to Article 5:80 Paragraph 2 of the Wft investment firms shall not be allowed to cooperate with the Offer;

(viii) no order, stay, judgment or decree having been issued prohibiting the Offer;

(ix) trading in the Shares not being suspended or ended by Euronext Amsterdam;

(x) no breach by either party to the merger agreement entered into by TenCate and the Offeror (the "Merger Agreement"), unless waived by the other party or remedied;

(xi) the irrevocable undertakings of Delta Lloyd Deelnemingen Fonds N.V., Delta Lloyd Levensverzekeringen N.V. and Delta Lloyd L European Participation Fund being in full force and effect and not having been breached or terminated, except as approved by the Offeror and TenCate; and

(xii) the Merger Agreement not having been terminated in accordance with its terms.

If and when made, the consummation of the Offer will be subject to the satisfaction or waiver of the following offer conditions:

(i) no material adverse change having occurred;

(ii) the aggregate number of (a) Shares tendered under the Offer, and (b) Shares directly or indirectly held by the Offeror or committed to the Offeror subject only to the Offer being declared unconditional, representing at least 95% of TenCate's issued share capital (geplaatst kapitaal) on a fully diluted basis as at the closing date of the Offer, excluding Shares held by TenCate or any of its group companies for its own account as at the closing date of the Offer (the "Minimum Acceptance Condition");

(iii) relevant competition clearances having been received or waiting and other time periods under applicable competition legislation or regulation having expired or lapsed;

(iv) any review or investigation by the Committee on Foreign Investment in the US ("CFIUS") having been concluded, and either: (i) the Offeror and TenCate having received written notice that a determination by CFIUS has been made that there are no unmitigated issues of national security of the United States sufficient to warrant further review or investigation pursuant to Section 721 of the Exon-Florio Amendment to the United States Defense Production Act of 1950, 50 U.S.C. app. § 2170, as amended; or (ii) the President of the United States shall not have acted pursuant to Section 721 of the United States Defense Production Act of 1950 to suspend or prohibit the consummation of the Offer, and the applicable period of time for the President of the United States to take such action shall have expired;

(v) a period of 60 calendar days having elapsed following notice under Section 122.4(b) of the U.S. International Traffic in Arms Regulations ("ITAR") to the U.S. Department of State (DDTC) of the Offer pursuant to the ITAR;

(vi) no initial public announcement having been made of (i) a Competing Offer (as defined and briefly described below) or (ii) a mandatory offer pursuant to article 5:70 of the Wft;

(vii) the Boards not having revoked, modified, amended or qualified their recommendation of the Offer;

(viii) no notification having been received from the AFM stating that pursuant to Article 5:80 Paragraph 2 of the Wft investment firms shall not be allowed to cooperate with the Offer;

(ix) no order, stay, judgment or decree having been issued prohibiting the Offer;

(x) trading in the Shares not being suspended or ended Euronext Amsterdam;

(xi) no breach by either party to the Merger Agreement, unless waived by the other party or remedied;

(xii) the extraordinary general meeting of Shareholders to be held during the acceptance period under the Offer (the "EGM") having adopted the following resolutions; (a) the granting of full release and full and final discharge to the members of the Boards until the date of the EGM, and (b) the appointment of three individuals identified by the Offeror as new members of the Supervisory Board; and

(xiii) the Merger Agreement not having been terminated in accordance with its terms.

The Offeror may waive or partially waive and lower the Minimum Acceptance Condition, unless the Minimum Acceptance Condition, following partial waiver and lowering, will be below 66 2/3%, in which case the prior approval of TenCate's Boards is required.

Competing Offer, Termination Fee

The Company and the Offeror may each terminate the Merger Agreement in the event that a bona fide third party makes an offer which, in the reasonable opinion of the Boards, is more beneficial, provided that the consideration per share exceeds the Offer Price by 7.5% (a "Competing Offer").

In the event of a Competing Offer, the Offeror will be given the opportunity to match such offer, in which case the Merger Agreement may not be terminated by the Company. As part of the Merger Agreement, the Company has entered into customary undertakings not to solicit third party offers.

If the Merger Agreement is terminated by the Offeror (i) following the announcement of a Competing Offer, or (ii) pursuant to the Boards having revoked, modified, amended or qualified their recommendation of the Offer in breach of the Merger Agreement, TenCate shall pay to the Offeror an amount equal to 0.75% of the aggregate consideration for all issued and outstanding Shares (the "Termination Fee").

Acquisition of 100%

The willingness of the Offeror to pay the Offer Price is based on the acquisition of 100% of the Shares. An acquisition of 100% enables termination of the listing and an efficient capital structure (both from a tax and financing perspective), which are important factors in achieving the premium implied by the Offer Price.

If the Offeror acquires 95% or more of the issued Shares, TenCate intends to delist from Euronext Amsterdam promptly and the Offeror intends to initiate the statutory squeeze-out proceedings to obtain 100% of the Shares.

If the Offeror acquires less than 95% of the Shares and decides, in its sole discretion, to waive the Minimum Acceptance Condition, the Offeror intends to utilise any legal measures available to it in order to acquire full ownership of TenCate (e.g. an asset transaction, statutory (cross border) merger or de-merger, contribution of assets and/or cash against issue by TenCate of additional shares).

The Offeror may acquire after settlement the entire business of the Company at the same price and for the same consideration as the Offer Price pursuant to an asset sale, followed by a liquidation of the Company, to deliver such consideration to Shareholders. Any such asset sale and liquidation will require the approval of the Executive Board and Supervisory Board, as well as the approval of the General Meeting of Shareholders.

Any measures (including a possible asset sale, followed by a liquidation of TenCate) shall require the approval of both Continuing Members of the Supervisory Board in the event that it could reasonably be expected to lead to a dilution of the shareholdings of the remaining minority shareholders of TenCate or any other form of unequal treatment which could prejudice or negatively affect the value of the Shares held by the remaining minority shareholders of TenCate.

Envisaged time schedule

TenCate and the Offeror will seek to obtain all necessary governmental approvals and competition clearances as soon as practicable. The required advice and consultation procedures with TenCate's Central Works Council and the relevant trade unions will start immediately.

The Offeror intends to launch the Offer as soon as practically possible and in accordance with the applicable statutory timetables. For further information explicit reference is made to the Offer Memorandum, which will contain further details regarding the Offer. The Offer Memorandum is expected to be published and the Offer is expected to commence in September or October 2015.

TenCate will hold an informative extraordinary general meeting of Shareholders at least 6 business days before closing of the offer period under the Offer, in accordance with Section 18 paragraph 1 of the Decree.

Advisors

ABN AMRO Bank N.V. and Rabobank are acting as financial advisors to TenCate and De Brauw Blackstone Westbroek N.V. is acting as legal advisor to TenCate. Allen & Overy is acting as legal advisor to the Supervisory Board. Hill+Knowlton Strategies is acting as communications advisor to TenCate.

ING Corporate Finance is acting as exclusive financial advisor to the Offeror. Clifford Chance is acting as legal advisor to the Offeror.

Further information

The information in this press release is not intended to be complete. For further information explicit reference is made to the Offer Memorandum, which is expected to be published in September or October 2015. This Offer Memorandum will contain further details regarding the Offer.

Slotkoers einde 2006 was EUR 23,21 en 2007 EUR 21,27

Wat premie? Nu de business de goede kant opgaat komen de haviken Red.XEA.nl.

tijd 09.18

Ten Cate EUR 24.125 +4,72 vol. 150.000